The financial technology sector has fundamentally rewritten the rules of engagement for global banking and lending. Not long ago, securing a loan was a bureaucratic marathon, defined by stacks of paperwork, manual verification, and the agonizingly slow deliberations of credit committees. For decades, the traditional banking system relied almost exclusively on static, backward-looking metrics—primarily centralized credit bureau scores like FICO.

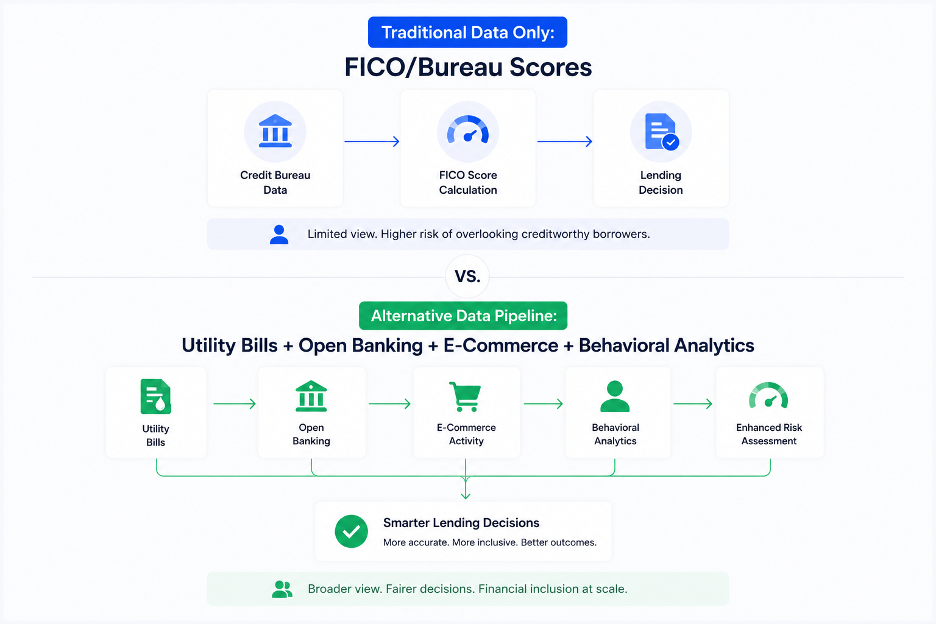

While these legacy systems served their purpose in a simpler economic era, they are increasingly obsolete in today's hyper-connected, fast-paced digital economy. The rigid nature of traditional scoring inherently excludes vast segments of the population, such as the unbanked, underbanked, gig-economy workers, and thin-file applicants who possess no formal credit history but are otherwise financially responsible.

Enter modern credit scoring software. Powered by Artificial Intelligence (AI), Machine Learning (ML), and big data analytics, these platforms have transformed underwriting from a reactive, historical autopsy into a predictive, real-time science. For FinTech companies looking to build these cutting-edge platforms, partnering with an experienced Custom software development provider has become a strategic necessity to ensure compliance, scalability, and robust algorithmic performance. By leveraging advanced data processing pipelines, FinTech lenders can now evaluate risk with unprecedented precision, making instantaneous, automated lending decisions that protect their portfolios while expanding market share.

The Flaws of Legacy Underwriting

To understand why modern credit scoring software is so revolutionary, one must first look at the structural vulnerabilities of traditional lending decisions. Legacy scoring models are fundamentally reactive. They take a snapshot of a borrower's financial past—typically looking at historical payment histories, existing debt ratios, and the length of credit accounts—and attempt to project future behavior.

This approach suffers from three major flaws:

- Data Latency: Credit bureau data is often updated only once a month, meaning lenders are frequently making multi-thousand-dollar decisions based on outdated financial snapshots.

- Binary Exclusion: Traditional models operate on a binary logic. If an applicant lacks a formal credit file, the system assigns a default high-risk score or rejects the application outright. This shuts out millions of creditworthy individuals globally.

- Inflexibility to Macroeconomic Shifts: Static scoring models struggle to adapt to sudden economic shocks, such as inflation spikes or labor market disruptions, leading to either over-exposure to bad risk or overly restrictive credit tightening.

FinTech platforms eliminate these bottlenecks by treating creditworthiness not as a static number, but as a dynamic, evolving behavioral profile.

The Power of Alternative Data and Big Data Ingestion

The cornerstone of modern credit scoring software is its ability to ingest, clean, and analyze vast amounts of non-traditional or "alternative" data. Rather than relying solely on whether a borrower paid off a credit card bill five months ago, FinTech software evaluates digital footprints that reflect real-time financial behavior.

When integrated into an advanced scoring engine, alternative data streams provide a holistic view of an applicant's financial life. Key data sources include:

1. Open Banking and Transactional Analytics

Through secure APIs, credit scoring software can directly access an applicant's checking and savings accounts (with their explicit consent). Machine learning algorithms parse raw transaction data in seconds, identifying recurring income streams, spending volatility, savings habits, and even micro-signals like overdraft frequencies or interactions with gambling platforms.

2. Utility and Telecom Payment Histories

Consistently paying utility, internet, and mobile phone bills on time is one of the strongest indicators of financial discipline. Modern scoring software automates the retrieval of this data, instantly legitimizing "thin-file" applicants who may not own a house or a traditional credit card but have years of unblemished utility payment records.

3. E-commerce and Merchant Data

For Small and Medium Enterprise (SME) lending, FinTech software connects directly to platforms like Amazon, Shopify, or Stripe. By analyzing real-time sales volumes, customer review sentiments, and inventory turnover rates, the software can judge the health of a business far better than a year-old tax return ever could.

4. Digital Behavioral Biometrics

Some highly advanced FinTech platforms analyze how an applicant interacts with the loan application interface itself. Factors such as the speed at which a form is filled out, whether information is copy-pasted (often a red flag for fraud), or the device type used, can be synthesized into subtle risk vectors.

Machine Learning: From Linear Regression to Deep Learning

At the heart of any sophisticated credit scoring platform lies the analytical engine. Traditional models rely heavily on logistic regression—a transparent but simplistic statistical method that evaluates variables in isolation. FinTech credit scoring software, however, leverages complex machine learning architectures, including Gradient Boosting Trees (like XGBoost), Random Forests, and Neural Networks.

As noted in recent deep dives on the Zfort Group Blog, the transition to ML-driven underwriting allows systems to identify intricate, non-linear relationships between hundreds of disparate variables simultaneously. For instance, a traditional model might see a sudden drop in a checking account balance as a pure risk factor. An ML model, however, can cross-reference that drop with a concurrent investment in inventory or a seasonal business cycle, correctly identifying it as a growth signal rather than financial distress.

Moreover, these models are self-learning. As loans are issued, matured, or defaulted upon, the software continuously feeds this performance data back into the system, automatically refining the weights of various scoring parameters to optimize future decision-making.

Mitigating Risk: Fraud Detection and Portfolio Health

Lending is ultimately a game of risk management. Credit scoring software does not just evaluate whether a borrower wants to pay back a loan; it determines the mathematical probability of default (PD) under various economic scenarios.

Beyond calculating credit scores, modern software acts as a robust firewall against identity theft, first-party fraud, and systemic portfolio risk.

Automated Fraud Detection

Fraudsters have become highly sophisticated, but credit scoring software uses device fingerprinting, geolocation tracking, and AI-driven identity verification (e-KYC) to spot anomalies instantly. If an applicant's behavioral data matches known patterns of synthetic identity fraud, the system automatically flags the application for manual review or triggers immediate rejection.

Dynamic Risk Pricing

Instead of a rigid "yes or no" decision, FinTech software enables dynamic risk pricing. Based on the exact probability of default calculated by the AI, the software can instantly customize the interest rate, loan amount, and repayment schedule for each individual borrower. This ensures that the lender is adequately compensated for taking on higher-risk profiles while offering highly competitive rates to prime borrowers.

Stress Testing and Portfolio Analytics

Advanced platforms allow risk officers to run macro-simulations across their entire loan portfolio. By altering software variables—such as predicting a 2% rise in unemployment—lenders can instantly see how their portfolio's default rate would shift, allowing them to adjust their automated underwriting thresholds proactively.

Balancing Innovation with Compliance: Explainable AI (XAI)

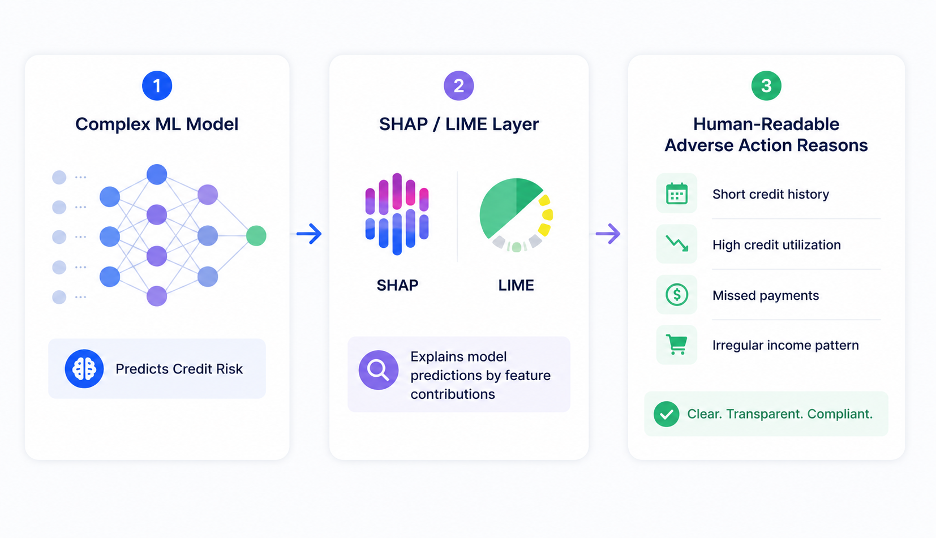

One of the biggest criticisms of early AI adoption in banking was the "black box" problem. Deep learning models could predict defaults with incredible accuracy, but they could not explain why a specific applicant was rejected. In a highly regulated industry governed by frameworks like the Fair Credit Reporting Act (FCRA) in the US or GDPR in Europe, this lack of transparency is a legal liability. Lenders are legally required to provide "adverse action notices," clearly stating the reasons for credit denial.

Modern credit scoring software solves this challenge through Explainable AI (XAI) frameworks, utilizing methodologies like SHAP (SHapley Additive exPlanations) and LIME (Local Interpretable Model-agnostic Explanations).

These mathematical layers break down complex algorithmic outputs into human-readable factors. If a model rejects an applicant, the XAI framework can pinpoint exactly which variables—such as a high debt-to-income ratio combined with volatile open-banking transactions—triggered the decision. This keeps FinTech platforms fully compliant with global fair-lending laws while retaining the predictive power of advanced AI.

Operational Efficiency and the Bottom Line

The business case for implementing dedicated credit scoring software is undeniable. For FinTechs and traditional banks alike, the metrics that dictate survival are the cost to acquire a customer (CAC), time-to-decision, and the non-performing loan (NPL) ratio.

| Performance Metric | Traditional Manual Lending | FinTech Scoring Software |

|---|---|---|

| Decision Time | 2 to 5 Business Days | 2 to 15 Seconds (Instant) |

| Data Points Analyzed | 10–15 (Bureau Only) | 1,000+ (Alternative + Bureau) |

| Operational Cost | High (Heavy Manual Review) | Low (Automated API-Driven) |

| Thin-File Approval | Extremely Low | High (Via Behavioral Profiling) |

By automating the underwriting pipeline, lenders can achieve Straight-Through Processing (STP) rates of over 80%. This means four out of five applicants receive an immediate approval or denial without a single human loan officer ever needing to touch the file. The operational savings are massive, allowing FinTechs to scale their loan volumes exponentially without a corresponding increase in headcount.

The Road Ahead: The Future of FinTech Underwriting

As we look toward the future, credit scoring software will only become more integrated, predictive, and pervasive. We are already seeing the emergence of decentralized finance (DeFi) protocols attempting to merge on-chain cryptographic data with off-chain credit metrics to facilitate under-collateralized crypto lending.

Furthermore, the continuous evolution of generative AI and natural language processing (NLP) will soon allow scoring software to analyze unstructured data—such as conversational patterns in customer support chats or the structural validity of business plans submitted by startups—to uncover hidden risk indicators.

However, software is not a silver bullet that can be set and forgotten. Financial ecosystems are living organisms. Models suffer from "data drift" and "concept drift" as economic conditions evolve, meaning that continuous monitoring, algorithmic auditing, and periodic retraining are vital to maintaining accuracy.

Ultimately, credit scoring software has democratized access to capital. By shifting the paradigm from rigid historical metrics to fluid, comprehensive behavioral analytics, FinTech lenders are not just making faster decisions—they are making fairer, smarter, and more profitable ones. In the hyper-competitive arena of modern finance, institutions that continue to rely on legacy underwriting will find themselves adverse-selected by lenders armed with superior algorithmic intelligence.

Executive Summary

- The Problem: Traditional credit scoring (like FICO) is reactive, relies on lagging data, and unfairly excludes "thin-file" borrowers like gig workers or SMEs.

- The FinTech Solution: Modern software leverages Big Data and Open Banking to analyze real-time alternative data (utility bills, cash flow, transaction histories).

- Advanced AI/ML: Machine Learning models recognize complex, non-linear risk patterns, enabling instant automated decisions and dynamic risk pricing.

- Compliance & Transparency: Explainable AI (XAI) frameworks unlock the "black box," ensuring compliance with fair lending laws by clarifying algorithmic rejections.

- The Bottom Line: Transitioning to AI underwriting slashes loan approval times from days to seconds, reduces operational costs, and minimizes default rates.